Data-driven solutions to meet your ISSB reporting obligations

The International Sustainability Standards Board (ISSB) provides a consistent framework for reporting sustainability metrics globally. It focuses on meeting information needs of investors, enables companies to disclose comprehensive sustainability information to global capital markets, and facilitates interoperability with other voluntary and mandated standards, such as the CSRD and US SEC.

As a wide-reaching global standard that is fast becoming a new norm for sustainability reporting, it directly impacts energy-intensive sectors like mining and resources today, and as it evolves.

Drawing on a decade of data-led process engineering and ESG reporting in the sector, this page breaks down the likely impact of the ISSB on resources operations, outlines the reporting requirements and outlines the latest digital tools available to help them prepare.

On 26 June 2023, the ISSB issued two international standards for investor-focused sustainability reporting: IFRS S1 covers General Requirements for the Disclosure of Sustainability-related Financial Information, and IFRS S2 covers Climate-related Disclosures. The standards intend to create a global baseline for sustainability-related financial disclosures.

Both standards are based on the four pillars used in the TCFD framework: governance, strategy, risk management, and sustainability-related metrics and targets. The standards refer to these four pillars as the ‘core content’.

As outlined by the IFRS, the two standards are designed to disclose information to capital markets and securities regulators about all material sustainability-related and climate-related risks and opportunities that could reasonably affect an entity’s cash flow, access to finance and cost of capital.

IFRS S1 is the General Standard, and IFRS S2 is the Climate Standard. In the future, more standards covering other topics are expected.

The ISSB standards have a single materiality focus, which means they focus only on the organisation’s financial impact. Standards like the CSRD, which have double materiality, focus on the financial impact as well as the external social and environmental impact.

The ISSB standards require reporting on sustainability-related financial disclosures. Impacts and dependencies are reportable only if they provide insights into a sustainability-related risk or opportunity that could reasonably affect a company’s prospects.

The ISSB standards became effective on 1 January 2024, and it is up to individual jurisdictions to adopt and mandate them.

The ISSB and the European Commission services, together with EFRAG, have worked together during the development of the European Sustainability Reporting Standards (ESRS) and the IFRS Sustainability Disclosure Standards (ISSB Standards) to achieve a high degree of alignment of the respective standards, with a specific focus on climate‑related reporting.

The ISSB has worked to achieve interoperability with other mandated standards, such as the CSRD and the US SEC requirements. This means organisations can report sustainability-related information using multiple frameworks without duplicating their efforts. Many resources are available to help organisations navigate this process.

Sustainability-related financial disclosures are required to be linked to a company’s financial statements to provide transparency about how sustainability-related factors impact the company’s financial performance and position.

This connection is crucial for investors and other stakeholders to understand the financial implications of sustainability-related risks and opportunities so they can make informed decisions.

Whether you are just starting your sustainability journey or already have sustainability reporting and compliance processes and targets in place, digital ISSB reporting software can help at every stage.

Starting by centralising your data, the right digital tools are the only way to address today’s mandatory requirements, adapt to evolving legislative frameworks, and help set and achieve decarbonisation targets.

For complex mining and minerals organisations, Metallurgical Systems recommends a staged approach to ISSB digital reporting that starts with meeting mandatory compliance rules and moves towards advanced capabilities and emissions reduction strategies as your ESG strategy matures.

Deploy ISSB reporting software to centralise data and use templates to meet today’s compliance regulations.

Set up the systems needed for centralised records that capture the in-depth ISSB data points needed to adjust to evolving ISSB reporting requirements.

On top of centralised data, the next step is to add automated data capture and data quality to your ISSB reporting.

This includes data cleansing, organisation and validation tools (using machine learning), and advanced visualisation tools to deliver dynamic, accurate and auditable near real-time ISSB reporting.

Beyond automation, the next step is enabling finance-grade sustainability reporting and automated validation of ISSB data against plant operations data using a mass and energy balance configured to your site/s.

You can report according to the ISSB reporting boundaries, time horizons (short, medium and long term) and extract reports in a machine-readable electronic format to meet ISSB requirements.

The final step is adding the granular analysis needed to plan, execute and evaluate your decarbonisation roadmap and adapt to evolving ISSB and sector-specific standards.

Running a steady-state simulation of your asset, validated finance-grade data is used to enable complex forecasting, transition planning, scenario analysis and climate resilience assessments.

You can then adjust inputs and compare final production, emissions and consumption using advanced visualisation tools.

For jurisdictions that have adopted the ISSB standards, they are relevant for companies and sectors, regardless of the financial reporting framework applied. They are not limited to companies reporting under the IFRS Accounting Standards.

Both the General Standard and the Climate Standard follow a structure consistent with the four pillars of the TCFD, reporting across areas of governance, strategy, risk management and metrics and targets. The structure of IFRS reporting will be familiar to those who already report under the TCFD.

Below, we break down the two primary standards:

AND

This Standard requires an entity to disclose information about all sustainability-related risks and opportunities that could reasonably be expected to affect the entity’s cash flows, its access to finance or cost of capital over the short, medium or long term. For the purposes of this Standard, these risks and opportunities are collectively referred to as ‘sustainability-related risks and opportunities that could reasonably be expected to affect the entity’s prospects’.

Topic Standards are the second component of the ISSB guidelines, focusing on specific sustainability topics. The first and only Topic Standard published to date is IFRS S2 Climate-related Disclosures.

AND

This Standard requires an entity to disclose information about climate-related risks and opportunities that could reasonably be expected to affect the entity’s cash flows, its access to finance or cost of capital over the short, medium or long term. For the purposes of this Standard, these risks and opportunities are collectively referred to as ‘climate-related risks and opportunities that could reasonably be expected to affect the entity’s prospects’.

Each ISSB standard requires specific disclosures to be reported. The IFRS Sustainability Disclosure Standards and IFRS Climate Disclosure Standard are based on the four pillars used in the TCFD framework: governance, strategy, risk management, and metrics and targets.

These four pillars are referred to as the ‘core content’. An entity must disclose material information concerning each of the four pillars.

Notably, the IFRS S2 (Strategy pillar) requires climate-related scenario analysis:

As per the IFRS S2 legislation: “An entity shall disclose information that enables users of general-purpose financial reports to understand the resilience of the entity’s strategy and business model to climate-related changes, developments and uncertainties, taking into consideration the entity’s identified climate-related risks and opportunities. The entity shall use climate-related scenario analysis to assess its climate resilience using an approach commensurate with its circumstances.”

It illustrates that if an entity has a high degree of exposure to climate-related risk, a more quantitative or technically sophisticated approach to climate-related scenario analysis would likely be required.

Of the four TCFD pillars, the ‘Metrics and targets’ pillar has a more quantitative focus. It requires organisations to disclose more granular metrics, including industry-based metrics such as GHG emissions broken down by types of gases and consumption data on water and energy.

Entities are required to report on any targets that they have set or are required to meet by the jurisdiction they operate in (by regulation or legislation). For each target, the entity is required to disclose any milestones or interim targets, performance against these targets, and an analysis of trends or changes in the entity’s performance.

The first table below summarises the core content, followed by a more detailed table detailing the IFRS S2 ‘metrics and targets’ disclosures.

While the standards include other information, this table summarises the requirements under the four pillars of the TCFD framework: governance, strategy, risk management, and metrics and targets. Together, they are referred to as the ‘core content’.

IFRS S1 Sustainability-related Disclosures

Governance

Strategy

Risk management

Metrics and targets

IFRS S2 Climate-related Disclosures

Governance

Strategy

Risk management

Metrics and targets

Note: See the table below for more details on IFRS S2 metrics and targets disclosures.

Cross-industry climate-related metrics

There are 7 cross-industry metrics:

Industry-based metrics

There are 68 volumes of industry-based guidance.

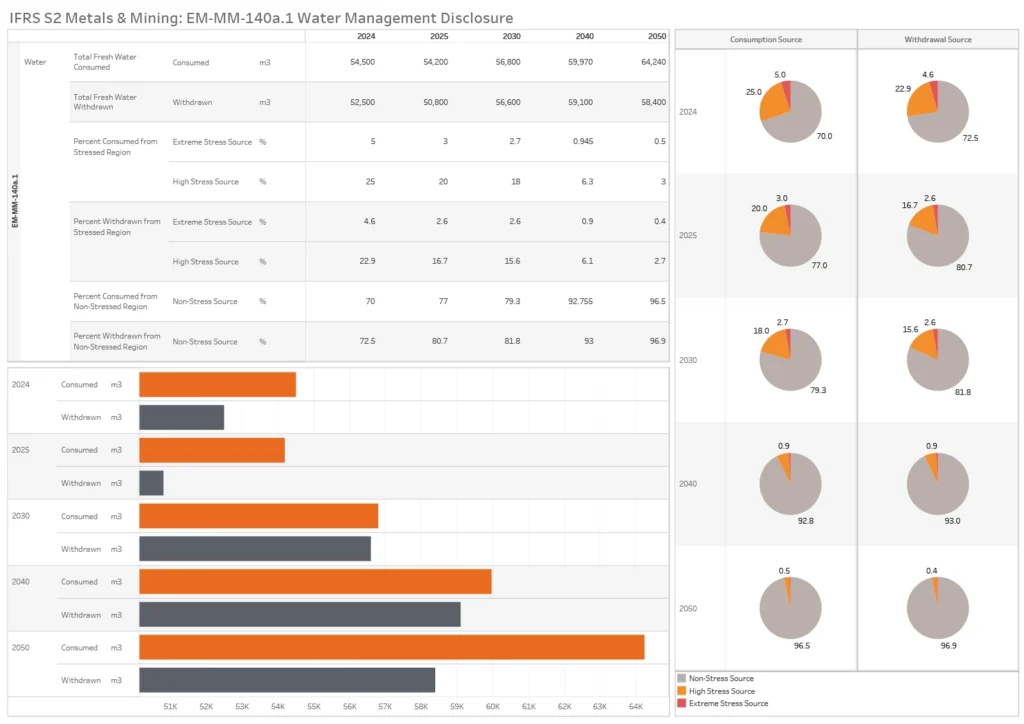

Below is an example of the “Metals and Mining” industry.

Sustainability disclosure topics and metrics include:

The need for regular reporting in a machine-readable digital taxonomy across hundreds of disclosures and the increasing requirement for detailed scenario analysis and forward-looking statements means that data-driven technology is the only solution to meet ISSB’s evolving sustainability disclosure rules and reporting standards.

Manual spreadsheets cannot capture or process the volumes of data needed to deliver immutable, unalterable and auditable sustainability reports.

The good news is that digital tools proven to solve these data challenges for complex industrial processes liking mining and resources are available.

MI Sustainability, as part of the Metallurgical Intelligence® suite of solutions, is an established platform that centralises plant-wide data and dynamically simulates your processing operation as a digital twin.

It performs a plant-wide mass and energy balance, and runs deep analysis across sustainability indicators, to deliver granular reports that are mapped to the IFRS Sustainability Disclosure Standard reference to be reported per the ISSB.

The following examples demonstrate how the MI Sustainability ISSB reporting software can satisfy ISSB compliance and help achieve decarbonisation goals with granular reports that map directly to the disclosures required.

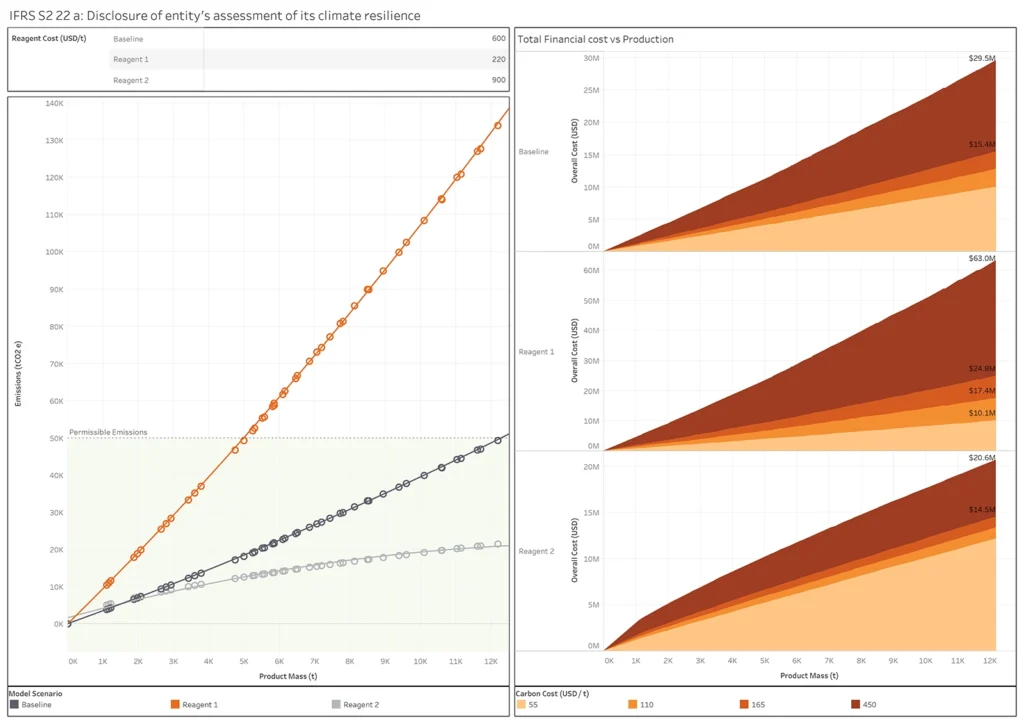

IFRS S2.22 requires an entity to use climate-related scenario analysis to assess its climate resilience, using an approach that is commensurate with its circumstances.

For entities with a high degree of exposure to climate-related risk, a quantitative or technically sophisticated approach to climate-related scenario analysis is required.

Here is an example of the use of quantitative climate scenario analysis as referenced in the Disclosure Requirement related to IFRS S2.22

Total emissions from using different reagents has been calculated compared to a set baseline, including the associated cost to the organisation. Using varying inputs under different climate scenarios, users of general purpose financial reports can understand the resilience of the entities strategy and business model.

There are seven cross-industry metric categories in IFRS S2.29 that include quantitative and qualitative components if material.

MI Sustainability can accurately measure and report Scopes 1, 2 and 3 across your value chain and adjust organisational boundaries as per the ISSB reporting requirements.

Scope 3 reporting is mandatory and can be broken down into categories.

Example of cross-industry metrics to be reported as per the IFRS S2.29 Disclosure of GHG emissions.

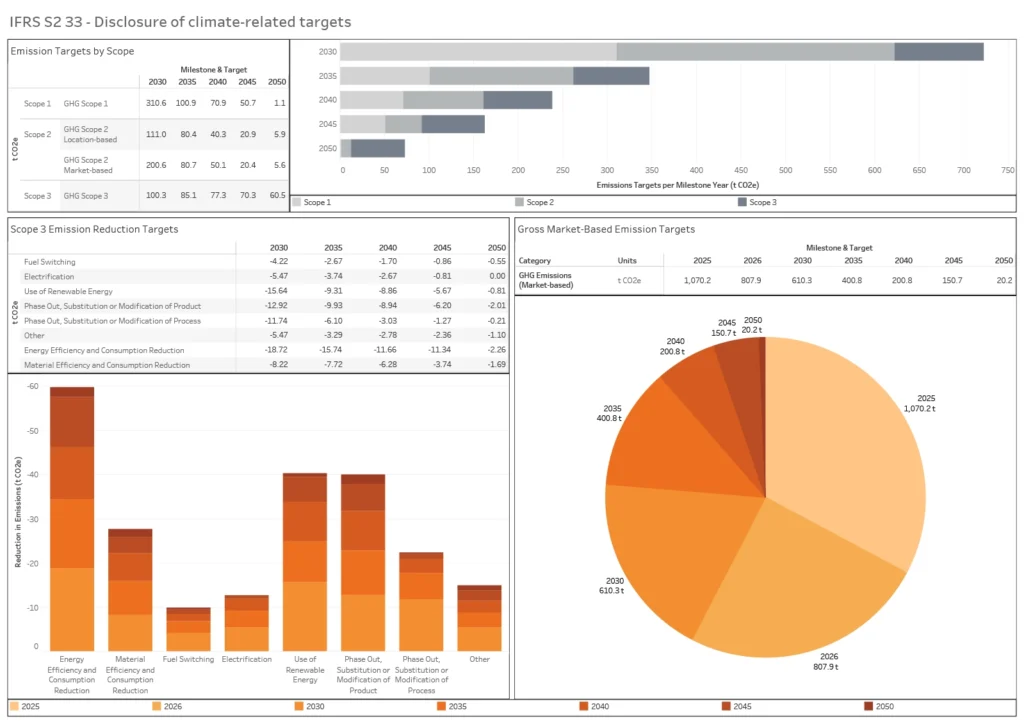

IFRS S2.33 and IFRS S2.34 requires an entity to disclose the quantitative and qualitative climate-related targets it has set, monitor progress towards set targets and any targets required by law or regulation.

For each target it is required to disclose how the latest international agreement on climate change, including jurisdictional commitments that arise from that agreement, has informed the target.

The entity is required to disclose information about its performance against each target and an analysis of trends or changes in the entity’s performance.

Here is an example of reporting on targets that MI Sustainability can automate such as the IFRS S2 33 –37, Disclosure of climate-related targets.

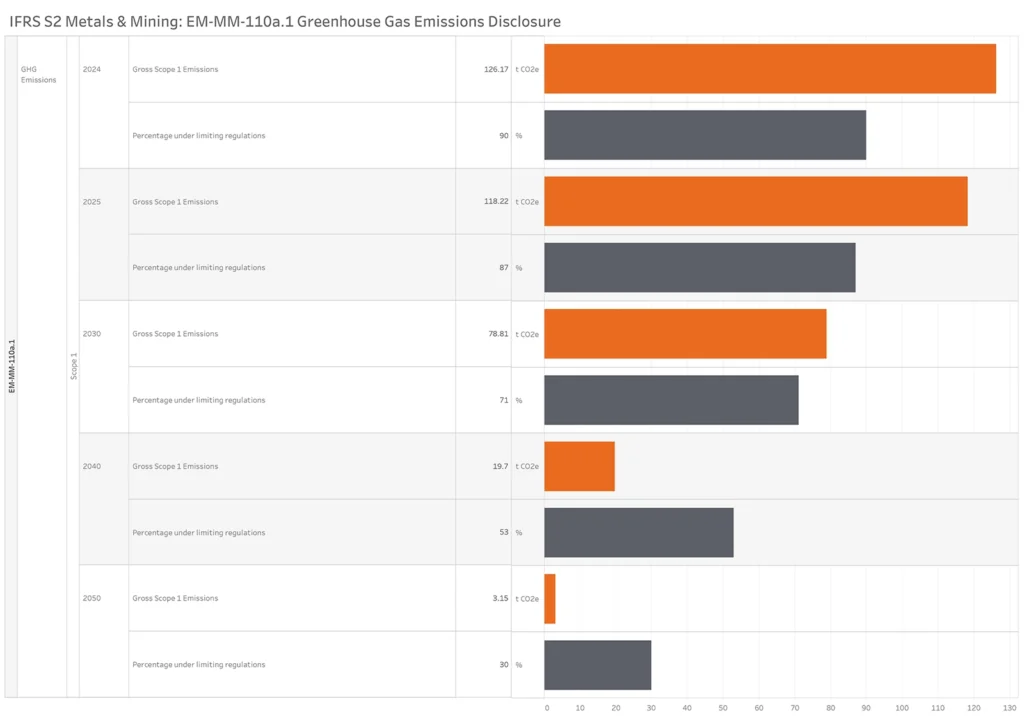

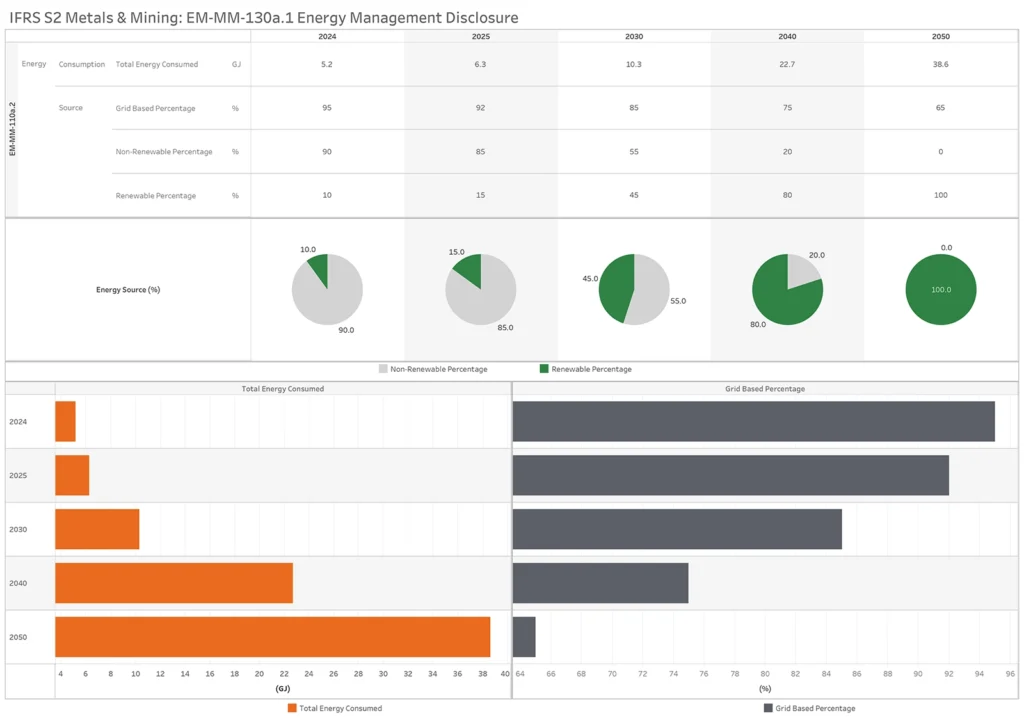

IFRS S2 requires an entity to disclose industry-based metrics that are associated with one or more particular business models, activities or other common features that characterise participation in an industry. In determining the industry-based metrics that the entity discloses, the entity shall refer to and consider the applicability of the industry-based metrics associated with disclosure topics described in the Industry-based Guidance on Implementing IFRS S2.

There are 68 volumes of industry-based guidance.

Sustainability Disclosure Topics & Metrics

Greenhouse Gas Emissions EM-MM-110a.1

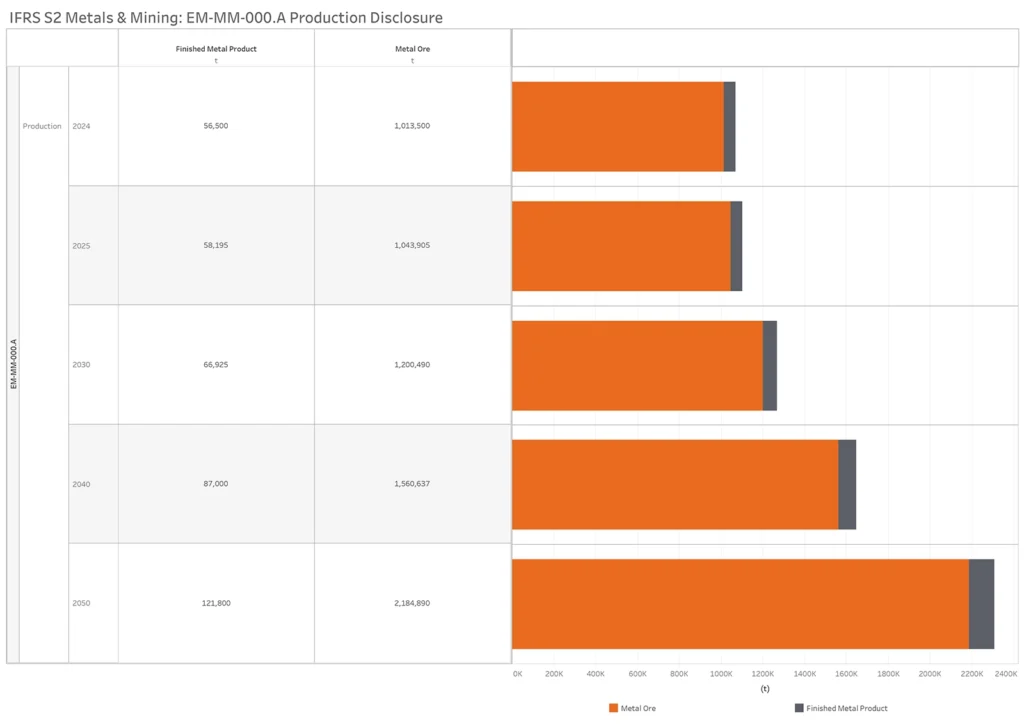

Activity Metrics

Production EM-MM-000.a

The International Auditing and Assurance Standards Board (IAASB) has proposed the International Standard on Sustainability Assurance 5000 (ISSA 5000), which provides general requirements for sustainability assurance engagements. Developed in collaboration with global and regional bodies, ISSA 5000 aims to establish a global baseline for sustainability assurance to improve the quality, accountability and transparency of sustainability information. The proposal closed for public consultation on December 2023, with final approval due September 2024.

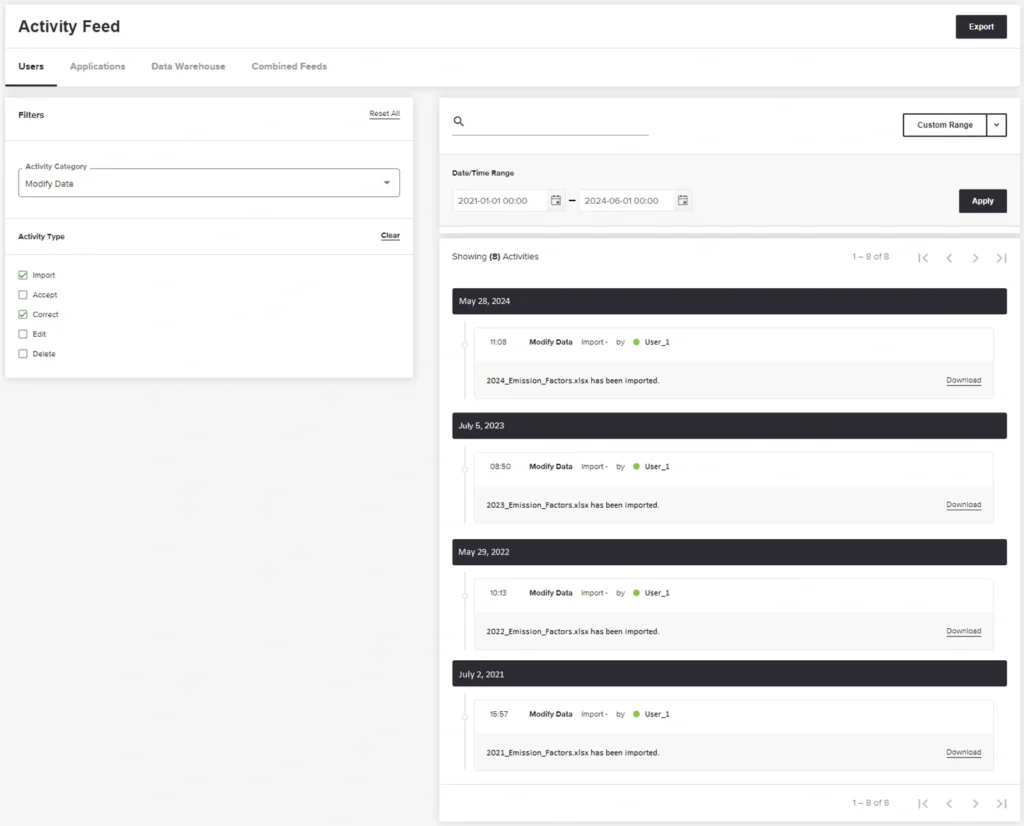

For complete assurance, organisations should demonstrate that they can track sustainability metrics back to source data such as instrumentation data and follow an audit trail to the reported values.

This is an example of the audit trail in the activity feed that details any changes or modifications to data.

ISSB published the IFRS Sustainability Disclosure Taxonomy (ISSB Taxonomy) on 30 April 2024.

Designed to be consistent with the IFRS accounting taxonomy the ISSB digital taxonomy can also be used with other digital taxonomies. MI Sustainability can map ISSB disclosures to digital tags as per the taxonomy.

The ISSB is an independent, global standard-setting body that develops and issues sustainability-related disclosure standards for companies to report on environmental, social, and governance (ESG) matters. It aims to promote transparency, consistency, and comparability in sustainability reporting.

The ISSB standards became effective on 1 January 2024, and it is up to individual jurisdictions to adopt and mandate them.

The ISSB standards have a single materiality focus, which means they focus just on the financial impact of the organisation. Standards like the CSRD that have a double materiality focus on the financial impact as well as the external social and environmental impact.

Compliance with the ISSB offers several benefits, including:

Companies that aren’t ready to meet their ISSB compliance regulations may face risks such as:

Many mining and minerals operations continue to use Excel spreadsheets to perform sustainability reporting. However, given the complexity of data, multiple data points and the requirement that reports be provided in an auditable electronic reporting format to be compliant, it’s become clear that Excel can no longer keep pace. Error-prone and time-consuming, using Excel exposes risks. Without the right data-driven sustainability platform, it’s impossible to meet ISSB reporting requirements, let alone implement effective decarbonisation strategies.

MI Sustainability simplifies ISSB reporting with a user-friendly interface, providing a comprehensive framework that covers all necessary disclosures. It automates data collection and calculation to reduce manual effort in producing reports in the ISSB digital format. It also enables companies to set targets, track progress, and benchmark performance.

To learn how MI Sustainability can help you meet your ISSB sustainability reporting obligations and minimise emissions, energy, water and waste across your supply chain, contact our expert team on +61 2 7229 5646 or info@metallurgicalsystems.com.

This article has been collaboratively authored by the team at Metallurgical Systems, and fact-checked and authorised by Managing Director and industry specialist John Vagenas.