Data-driven solutions to meet your CSRD reporting obligations

Calls for transparent sustainability reporting in heavy industries like mining and resources have been growing louder in recent years. However, emerging regulations such as the CSRD have moved it from a voluntary nice-to-have to a mission-critical mandatory activity with significant consequences.

Drawing on over 10 years of experience in process engineering, data-led software and sustainability reporting in the resources sector globally, Metallurgical Systems can help you understand how the CSRD impacts your organisation and share digital tools to make sure you’re ready.

For business leaders and CFOs, now is the time to prepare for CSRD to protect and grow your operations, financials and reputation.

Organisations must disclose the impacts, risks, and opportunities (IRO) deemed material under these standards from the company and stakeholder perspectives.

The CSRD was adopted by the European Parliament and the European Council in November 2022 and entered into force on 5 January 2023. As of 1 January 2024, at least 50,000 companies operating in the EU must comply with the new CSRD rules and publish sustainability disclosures in their 2024/2025 financial reports.

The CSRD includes two cross-cutting standards and ten topic standards of the European Sustainability Reporting Standards (ESRS), including climate change, pollution and other aspects of corporate sustainability.

As reported by the European Council, sector-specific standards will become effective on 30 June 2026. This allows companies more time to focus on implementing the first set of ESRS.

Specific sectors will likely be oil and gas, coal, quarries and mining, road transport, agriculture, farming and fisheries, motor vehicles, energy production and utilities, food and beverages, textiles, accessories, footwear and jewellery.

Double materiality assessment is crucial for CSRD compliance. This means companies need to report on both the impact of the organisation’s activities on society and the environment (impact materiality) and the effects of the environmental, social and governance (ESG) factors on the financial position of the company (financial materiality).

Organisations must start preparing their data and systems to meet their reporting and complaint obligations.

Whether you are just starting your sustainability journey or already have sustainability reporting and compliance processes and targets in place, digital CSRD reporting software can help at every stage.

Starting by centralising your data, the right digital tools are the only way to address today’s mandatory requirements, adapt to evolving legislative frameworks, and help set and achieve decarbonisation targets.

For complex mining and minerals organisations, Metallurgical Systems recommends a staged approach to CSRD digital reporting that starts with meeting mandatory compliance rules and moves towards advanced ESG capabilities and emissions reduction strategies as your capabilities mature.

Deploy CSRD reporting software to centralise data and use templates to meet today’s compliance regulations.

Set up the systems needed for centralised records that capture the in-depth CSRD data points needed to adjust to evolving CSRD reporting requirements.

On top of centralised data, the next step is to add automated data capture and data quality to your CSRD reporting.

This includes data cleansing, organisation and validation tools (using machine learning), and advanced visualisation tools to deliver dynamic, accurate and auditable near real-time CSRD reporting.

Beyond automation, the next step is enabling finance-grade sustainability reporting and automated validation of CSRD data against plant operations data using a mass and energy balance configured to your site/s.

You can report according to the CSRD reporting boundaries, time horizons (short, medium and long term) and extract machine-readable format to deliver the required CSRD electronic formats.

Decarbonisation roadmap

The final step is adding the granular analysis needed to plan, execute and evaluate your decarbonisation roadmap and adapt to evolving CSRD and sector-specific standards.

Running a steady-state simulation of your asset, validated finance-grade industrial data is used to enable complex forecasting, transition planning, scenario analysis and climate resilience assessments.

You can then adjust inputs and compare final production, emissions and consumption using advanced visualisation tools.

The CSRD reporting format is based on the European Sustainability Reporting Standards (ESRS), which provide a framework for companies to report on their sustainability performance consistently and comparably. The first set of ESRS was published on 22 December 2023.

These standards apply to companies under the scope of CSRD regardless of the sector in which they operate.

There are three categories of ESRS reporting:

These standards, including ESRS 1 and ESRS 2, set the foundation for sustainability reporting requirements. They are mandatory and apply to all companies reporting under CSRD.

These standards provide specific reporting requirements for a range of environmental, social and governance (ESG) topics, including climate change, human rights and biodiversity. They are designed to help companies report on their impact and performance in specific areas and are only reported if they are assessed as material.

If a company deems topic standard ESRS E1 immaterial in the CSRD reporting scope, and omits the disclosure requirements, the report must include a detailed explanation of the materiality assessment’s conclusions. This includes a forward-looking analysis of the conditions that could lead the company to conclude that this topic standard ESRS E1 is material in the future.

Other topic standards deemed immaterial do not require a detailed explanation. However, the company may mention the negative materiality assessment under standards ESRS 2 IRO-2, General disclosures.

E1 – Climate change

E2 – Pollution

E3 – Water & marine resources

E4 – Biodiversity & ecosystems

E5 – Resource use and circular economy

S1 – Own workforce

S2 – Workers in own value chain

S3 – Affected communities

S4 – Consumers & end-users

G1 – Business conduct

While details are not yet released, these standards will provide additional guidance for companies in specific industries, such as finance or manufacturing, to report on sector-specific sustainability issues and impacts. These will help companies address industry-specific risks and opportunities.

Each ESRS Disclosure Requirement requires one or more specific data points to be reported. This includes all the data points from ESRS 2 and the topical standards. There are no specific data point disclosure requirements for ESRS 1 General Requirements.

EFRAG released the draft list of ESRS data points in December 2023. This presents the complete list of the detailed requirements contained in each Disclosure Requirement and related Application Requirements. The list organises and categorises narrative and quantitative disclosures, making it a valuable resource for adapting to a new reporting standard or forming the basis of a data gap analysis.

ESRS 2 General disclosures

16 Disclosure requirements

195 Data points

ESRS G1 Business conduct

7 Disclosure requirements

53 Data points

ESRS S1

Own workforce

18 Disclosure requirements

202 Data points

ESRS S2

Workers in the value chain

6 Disclosure requirements

72 Data points

ESRS S3

Affected communities

6 Disclosure requirements

71 Data points

ESRS S4

Consumers and end-users

6 Disclosure requirements

70 Data points

ESRS E1

Climate change

12 Disclosure requirements

220 Data points

ESRS E2

Pollution

7 Disclosure requirements

68 Data points

ESRS E3

Water and marine resources

6 Disclosure requirements

48 Data points

ESRS E4

Biodiversity and ecosystems

8 Disclosure requirements

120 Data points

ESRS E5

Resource use and circular economy

7 Disclosure requirements

84 Data points

The need for regular reporting in a machine-readable digital taxonomy across hundreds of specific data points and the increasing requirement for detailed scenario analysis and forward-looking statements means that data-driven technology is the only solution to meet CSRD’s evolving sustainability disclosure rules and reporting standards.

Manual spreadsheets cannot capture or process the volumes of data needed to deliver immutable, unalterable and auditable sustainability reports.

Complex industrial processes liking mining and resources require a specialised approach to sustainability reporting like the CSRD. The need for a granular mass balance tracking at every step of the production process across the value chain demands advanced digital tools.

The good news is that digital tools that have been proven to solve these data challenges for complex mining and minerals operations.

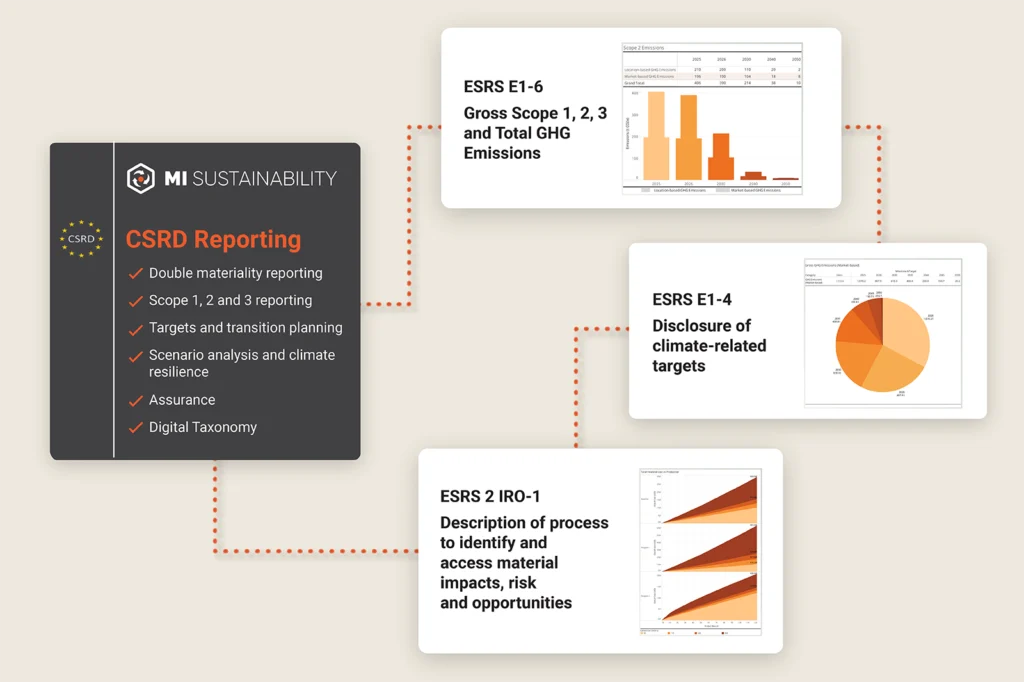

MI Sustainability, as part of the Metallurgical Intelligence® suite of solutions, is an established platform that centralises plant-wide data and dynamically simulates your processing operation as a digital twin. It performs a plant-wide mass and energy balance and delivers granular reports and deep analysis across sustainability indicators to comply with evolving global frameworks including the CSRD.

These examples demonstrate how the MI Sustainability CSRD reporting software and solutions can satisfy CSRD compliance and help achieve decarbonisation goals with granular reports that map directly to the data points required by the ESRS.

CSRD requires companies to measure sustainability data points to evaluate impact and financial materiality in one platform with historical comparisons.

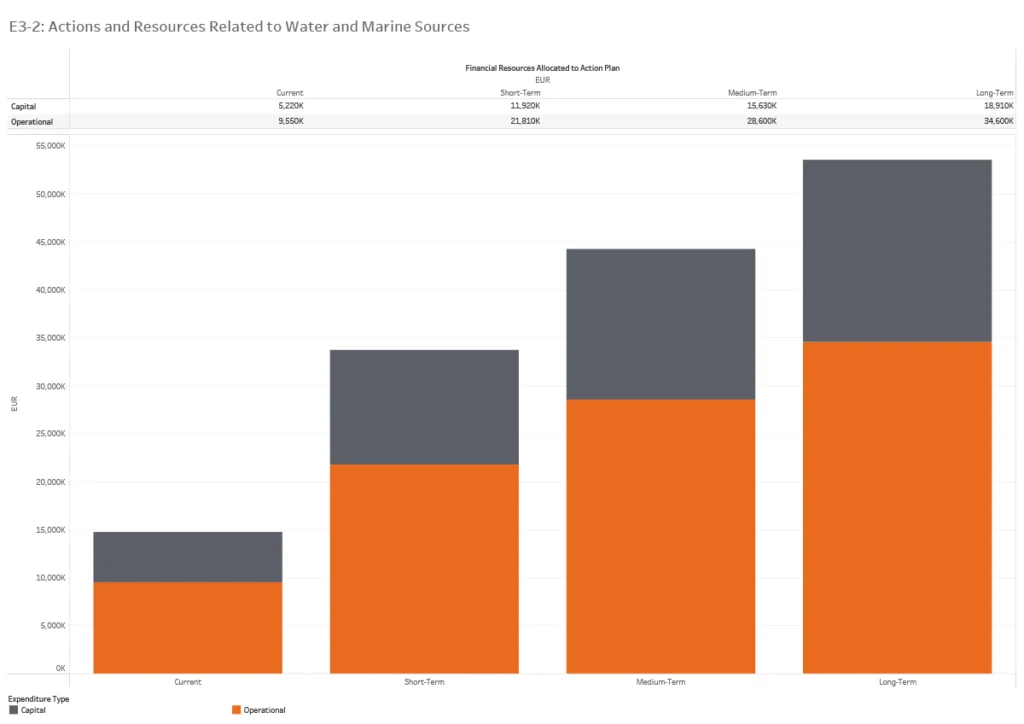

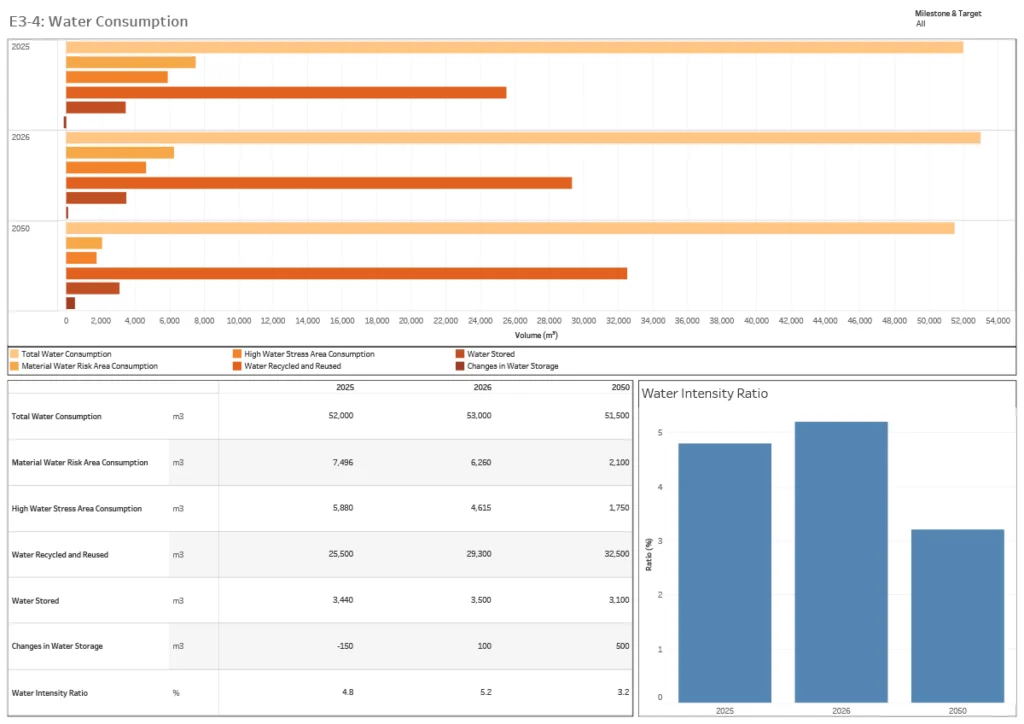

In this example we demonstrate how MI Sustainability reports on financial resources allocated as well as the impact measurement of water consumption.

Example data points to be reported as per ESRS E3-2. Disclosure of water and marine resources-related actions and resources allocated to their implementation.

Example data points to be reported as per ESRS E3-4. Disclosure of information about water consumption performance related to material impacts, risks and opportunities.

MI Sustainability can accurately measure Scopes 1, 2 and 3 across your value chain and adjust organisational boundaries as per the CSRD reporting requirements.

Scope 3 reporting is mandatory and can be broken down into categories.

Gross Scope 1,2,3 and Total GHG Emissions Report:

Example of data points to be reported as per the ESRS E1-6. Disclosure of GHG emissions.

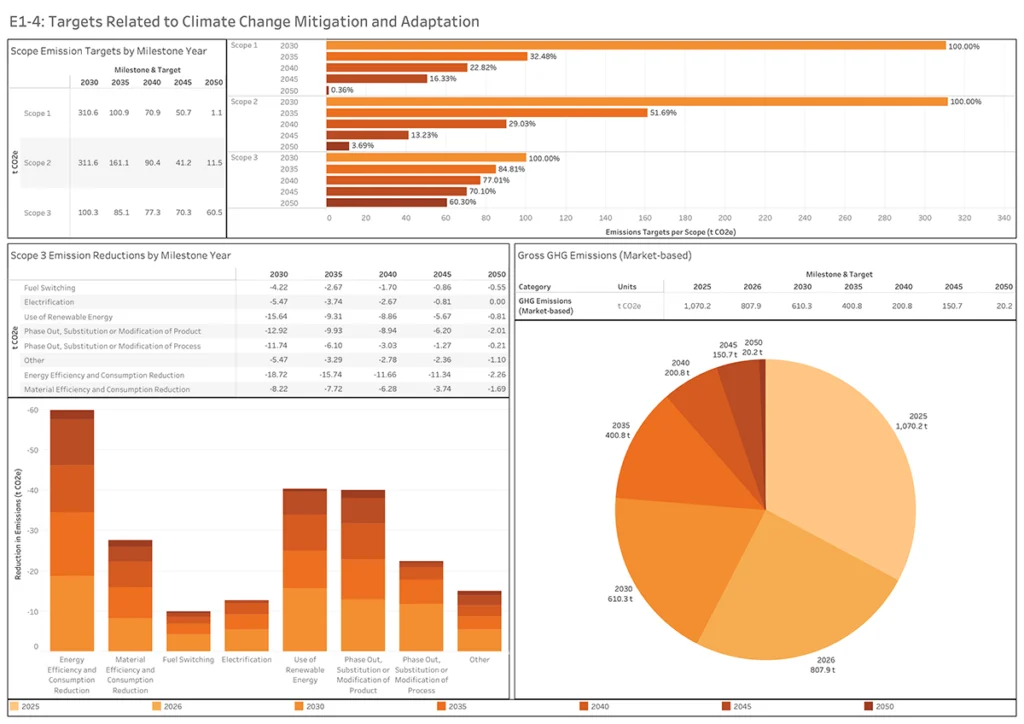

CSRD requires disclosure of transition plans compatibility with the most recent international agreement on climate change.

This includes disclosure on GHG emissions reduction targets in five-year rolling periods, including targets set for 2030 and 2050 if available.

Here is an example of the milestone data points that need to be reported as per the CSRD ESRS E1-4 that MI Sustainability can automate. Disclosure of climate-related targets.

CSRD requires companies to conduct scenario analysis to evaluate their climate resilience and explain how their strategies align with the Paris Agreement’s goals.

Climate resilience refers to a company’s ability to adapt to climate change and its related challenges and opportunities.

This includes managing risks, responding to changes, and taking advantage of new opportunities, both strategically and operationally.

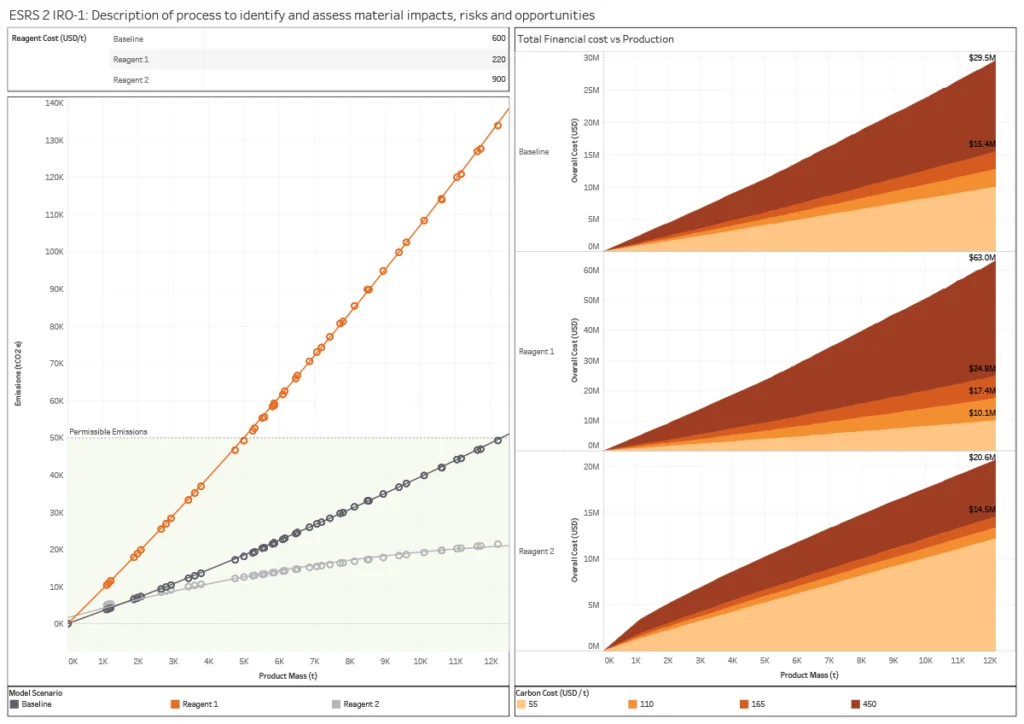

Here is an example of the use of quantitative climate scenario analysis as referenced in the Disclosure Requirement related to ESRS 2 IRO-1.Total emissions from using different reagents has been calculated compared to a set baseline, including the associated cost to the organisation.

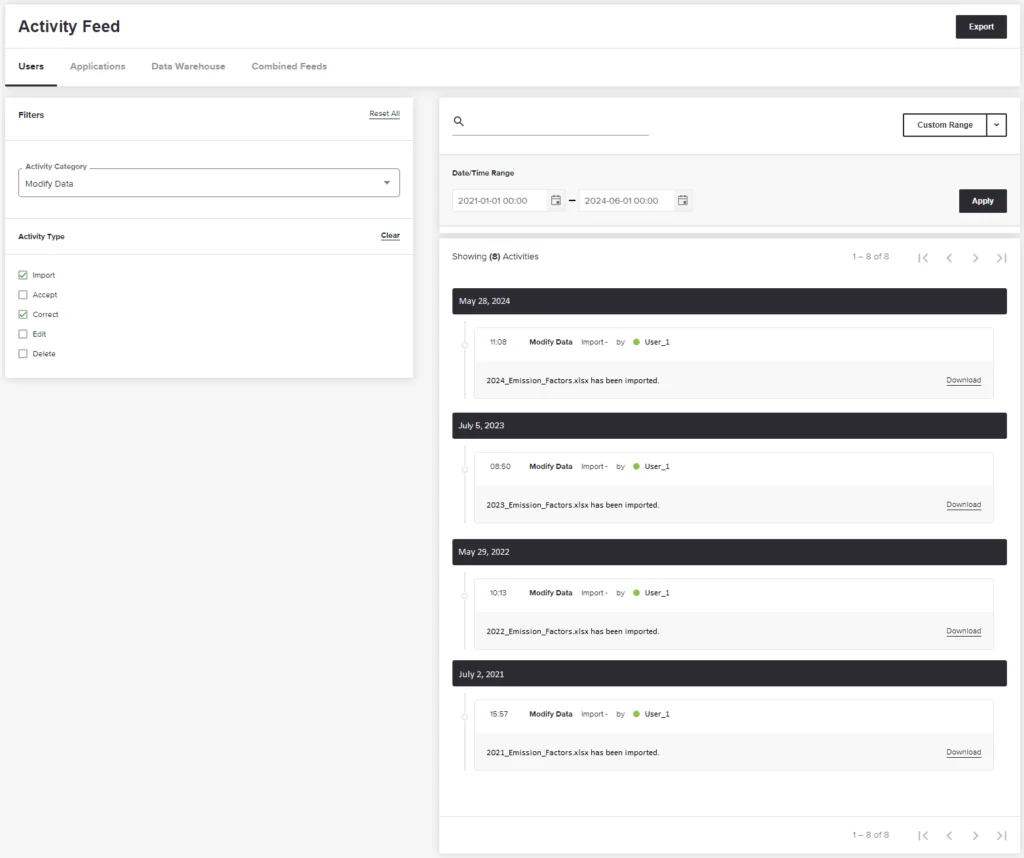

CSRD requires organisations to track sustainability metrics back to source data such as instrumentation data and follow an audit trail to the reported values.

This is an example of the audit trail in the activity feed that details any changes or modifications to data.

CSRD requires management reports to be submitted in accordance with the CSRD electronic reporting format.

European Financial Reporting Advisory Group (EFRAG) has developed a digital XBRL taxonomy. MI Sustainability can map source data to digital tags as per the taxonomy.

Put simply, the CSRD, or Corporate Sustainability Reporting Directive, is a European Union regulation that mandates sustainability reporting for a broader range of companies. It aims to improve transparency and accountability on environmental, social and governance (ESG) issues.

The CSRD was adopted in November 2022 and took effect on 5 January 2023. Starting 1 January 2024, at least 50,000 EU-based companies must follow the new CSRD rules and include sustainability information in their 2024/2025 financial reports.

The provisions of the CSRD are broad in scope and apply to many companies operating in the EU, estimated to be nearly 50,000 in total. They will increasingly apply to a significant number of SMEs (small and medium-sized enterprises).

Companies must report on a comprehensive range of ESG factors using the European Sustainability Reporting Standards (ESRS). This includes environmental impacts like climate change and pollution, social aspects like labour practices and diversity, and governance issues like business ethics and anti-corruption measures.

The CSRD emphasises the concept of double materiality. Companies need to report on sustainability factors that are both material to their business (financial impact) and those that significantly impact people and the environment (external impact).

Compliance with the CSRD offers several benefits, including:

Companies that aren’t ready to meet their CSRD compliance regulations may face risks such as:

Many mining and minerals operations continue to use Excel spreadsheets to perform sustainability reporting. However, given the complexity of data, multiple data points and the requirement that reports need to be provided in an auditable electronic reporting format to be compliant, it’s become clear that Excel can no longer keep pace. Error-prone and time-consuming, using Excel exposes risks. Without the right data-driven sustainability platform, it’s impossible to meet CSRD reporting requirements, let alone implement effective decarbonisation strategies.

MI Sustainability simplifies CSRD reporting with a user-friendly interface, providing a comprehensive framework that covers all necessary disclosures. It automates data collection and calculation to reduce manual effort to produce reports in the required CSRD digital format. MI Sustainability also enables companies to set targets, track progress and benchmark performance.

Designed to navigate multiple global frameworks and many separate ESG performance indicators, MI Sustainability is a uniquely flexible and comprehensive sustainability reporting solution for today and the future.

Whether you are just starting your sustainability journey or already have sustainability reporting and compliance processes and targets in place, MI Sustainability has flexible packages for every stage.

It adapts to the needs of your operation from simply ticking sustainability compliance boxes through to advanced environmental, social and governance (ESG) capabilities:

To learn how MI Sustainability can help you automate your CSRD sustainability reporting and compliance, streamline processes and minimise emissions, contact our team of engineers, metallurgists and technology professionals on +61 2 7229 5646 or info@metallurgicalsystems.com.

This article has been collaboratively authored by the team at Metallurgical Systems, and fact-checked and authorised by Managing Director and industry specialist John Vagenas.